How community banks can help young homebuyers

Photo by Ridofranz/iStock

As house prices skyrocket, student loan debt grows and wages stagnate, many Gen Zers and millennials are watching their homebuying dreams move out of reach. But there are ways community banks can help mortgage-seekers get on the property ladder.

By Beth Mattson-Teig

Millennial and Gen Z borrowers chasing the American Dream of buying that first home are facing stiff obstacles amid inflationary pressures, soaring home costs and, for many, a staggering burden of student loan debt.

Frankly, say observers, it is getting tougher to make the numbers work for a variety of first-time homebuyers—regardless of age.

“I don’t think the issue is a lack of financing alternatives,” says Ron Haynie, ICBA’s senior vice president of mortgage finance policy. “There is ample supply of credit. It’s a question of the supply of affordable properties that first-time homebuyers can get into and buy.”

Median home prices have been rising at a double-digit clip, including a 15.7% year-over-year increase in the first quarter of 2022, according to the National Association of Realtors (NAR). Mortgage rates are also rising for the first time in a while, with the 30-year fixed-rate mortgage hovering at 5.5% in early May—up nearly 250 basis points from lows around 3% seen in 2021. That increase in mortgage rates has a big impact on what a buyer can afford, notes Haynie. “So, there are a lot of headwinds against first-time buyers.”

The student loan challenge

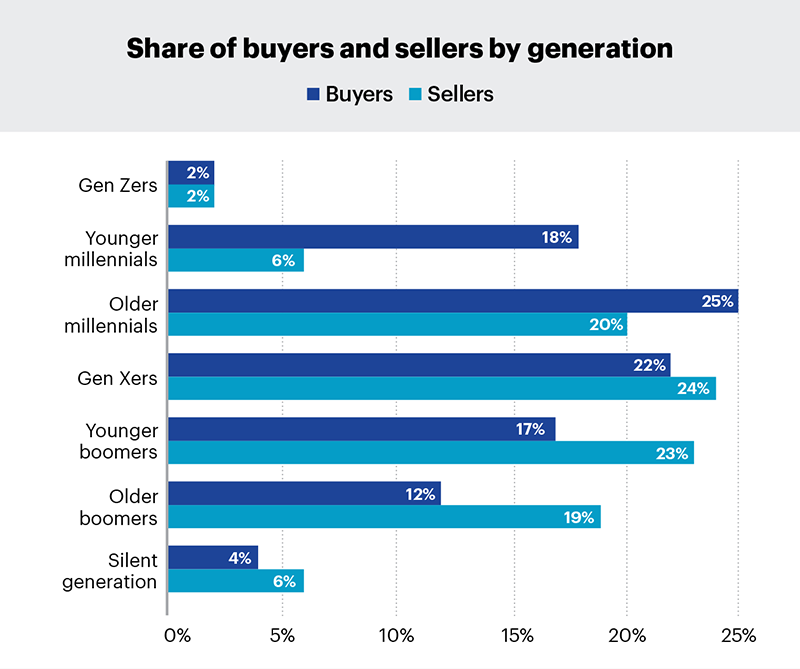

According to the 2022 Home Buyers and Sellers Generational Trends Report published by the NAR, there are some clear generational trends in the homebuying market. Younger millennials and Gen Z buyers—those born after 1980—represent 45% of the total homebuyer market.

An added challenge for those younger prospective homebuyers is a heavy load of student debt that puts added pressure on monthly budgets. More than 43 million Americans hold student loans; the combined volume of student debt has almost doubled over the past decade to $1.75 trillion, according to the Education Data Initiative.

“Definitely, student loans can be an issue for some people, especially for those individuals who come out of college with jobs that are not equal in pay to what they have in student loan debt,” says Mark A. Burmis, senior vice president and retail lending manager at $450 million-asset Chelsea State Bank in Chelsea, Mich.

So how can community banks help? They can step in to assist first-time homebuyers of all ages with educational resources and financial counseling. The relationship banking model allows community bankers to have conversations with prospective borrowers about whether they’re ready to buy, how much they can afford to buy, and if they even want to buy now when home prices could be near a peak.

“That can be a tough conversation to have,” says Haynie. With the hot housing market, it is important to counsel customers so they think about all the potential factors and don’t get caught up in a bidding war or get in over their heads, he says.

Click to enlarge

Click to enlarge

Source: 2022 Home Buyers and Sellers Generational Trends, National Association of Realtors

Plenty of tools in the box

For customers who decide buying is the right choice, community bankers have a variety of products and services available to help. For banks selling loans in the secondary market, options include loan products available through the Federal Housing Authority, Freddie Mac and Fannie Mae that offer lower down payments, competitive rates and flexibility on qualifying. Federal Home Loan Banks, as well as state and local housing finance agencies, also provide grant programs for qualifying buyers to assist with down payments and closing costs.

Chelsea State Bank offers loans through Freddie Mac’s HomeOne and Fannie Mae’s HomeReady programs, says Burmis. The community bank also hopes to participate in a new tax-exempt savings program for first-time homebuyers that was approved by the state of Michigan in April. The new law allows individuals to set aside money for a home purchase down payment, and money saved via the program is free from state income tax. Starting in 2022, single participants will be eligible to receive up to a $5,000 deduction each year and $10,000 for joint filers, as long as their maximum account balance does not exceed $50,000. “It’s all about helping customers the best that we can,” says Burmis.

Mansfield, Ohio-based Mechanics Bank offers a number of mortgage options for loans it holds in its portfolio. One of these is the 10/1 ARM, which offers a fixed rate for the first 10 years of the loan, after which it shifts to a variable rate. According to Mark Masters, president and CEO of the $805 million-asset community bank, one of the reasons the product is popular is because most buyers make a change within that first decade. Perhaps they sell and move to another home, or they refinance the existing loan to pull out equity and make improvements.

“It’s very attractive to first-time homebuyers, because it offers a lower rate, a lower payment and the flexibility they need,” says Masters.

Flexibility needed

Community banks that are going to hold a loan in their portfolio have more flexibility in the underwriting and structure. And although banks follow fair lending laws and don’t offer special treatment for younger borrowers, flexibility can be beneficial for millennial and Gen Z customers who have embraced the “gig economy” of non-W-2 income. “If you’re self-employed or have several different things that you do, sometimes it’s more difficult to get qualified for a secondary market mortgage,” says Haynie. “That’s where our members as portfolio lenders have an advantage, because they are able to look at the situation in a broader context.” Obviously, all banks have a credit policy, he adds, but they can also choose what they will accept for verification of income.

For example, Mechanics Bank does not base its loan decisions on credit scores. “Credit experience is important to us,” says Masters. “However, there is more of an opportunity for us to help first-time homebuyers than they might find elsewhere, because we’re not just focused on this one number, the credit score.”

The community bank’s lenders listen to the borrower’s story and take their whole situation into account. “It’s not just about their income and their debt and their credit history; it’s about other things that are contributing to their life in general,” Masters says. “Once we hear their story, we understand their obligations.” For example, if a borrower is in an entry-level job, their income has the potential to increase, he notes.

Providing educational resources

First-time homebuyers face a steep learning curve when it comes to the mortgage process, so community bankers have an opportunity to deepen relationships by providing informational resources online, in person and through educational seminars. Chelsea State Bank partnered with a local title company and realtor to host a first-time homebuyer seminar in April that covered a variety of topics, such as budgeting, how to improve credit, down payments, debt-to-income ratios and available homeownership grants.

Budgeting is especially important for first-time homebuyers, notes Burmis. Some of the loan programs available through Fannie and Freddie will allow people to go up to 50% debt-to-income (DTI) on their total back-end ratio, which includes all of one’s debt. What that means is if an individual makes $5,000 per month, $2,500 can go to payments such as student loans, car loans and the mortgage. However, it is also important for the customer to think about expenses that are not included in that DTI calculation, such as car insurance, income taxes, phone bills, groceries and 401(k) investments.

“At the end of the day, 50% DTI might be a little bit too high for a particular individual, but it can be approved,” says Burmis.

While the borrower needs to be the one to set their budget, the lender can provide some guidance on what a prudent number is, or what other expenses need to be considered along with the DTI when budgeting, notes Burmis. Chelsea State Bank hopes to hold additional seminars in the future. “We’re trying to be more focused on financial literacy in the communities we serve, and we believe that if we can help our communities to be more educated, the whole community will prosper and benefit from it,” he adds.

Other helpful resources community banks can provide include online tools, such as mortgage calculators, that appeal to customers of all ages. However, the best thing community banks can do is talk to customers about their unique situation and their goals for buying a home now or at some point in the future.

At Mechanics Bank, even if the bank decides it can’t make the loan, lenders take the time to explain why. For example, if a loan applicant has an abundance of credit card debt inhibiting their ability to borrow, lenders can help them through credit counseling services, or perhaps restructure that debt, so that at some point they will be in a better position to buy their first home, he says.

Hopefully, adds Masters, that borrower will return to the bank when they are in a stronger position and the bank will be able to make the loan.

Tips for creating educational resources

Millennial and Gen Z homebuyers do their homework, and their first stop for research is often online. Community banks need to offer online resources and tools, such as online mortgage calculators and FAQs, that can help answer questions and serve that appetite for information.

The Consumer Finance Protection Bureau offers a variety of information and resources that are helpful for both homebuyers and bankers looking to create more educational content to assist customers.

Beth Mattson-Teig is a writer in Minnesota.

Comments are closed.